There’s no one right way to budget, so long as you’re managing your spending and achieving your financial goals in a sustainable way. Choosing the right budget for your personality and lifestyle is crucial to making your finances work for you, which is why Monarch offers the choice between flex and category budgeting.

Flex and category budgeting take different approaches to organizing your finances.to organizing your finances. Whereas category budgeting focuses on detailed limits for individual category types, a flex budget offers a “big picture” view by assigning expenses to one of three big categories.

Choosing the method that’s right for you will depend on your priorities and your financial management style. Monarch has the tools to help you build a category or flex budget that truly fits your style, and to build it into your larger financial plan for your household. Here’s what to know about both budgeting methods.

What is Flex Budgeting?

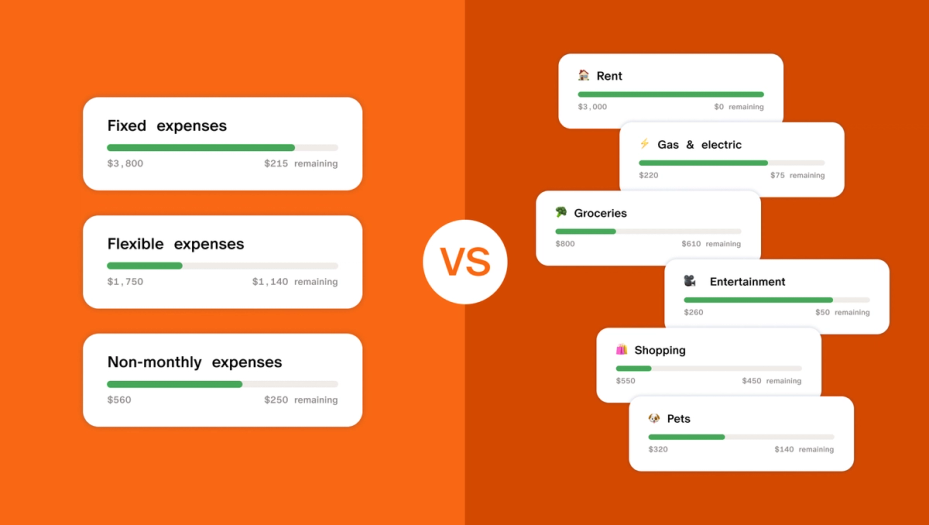

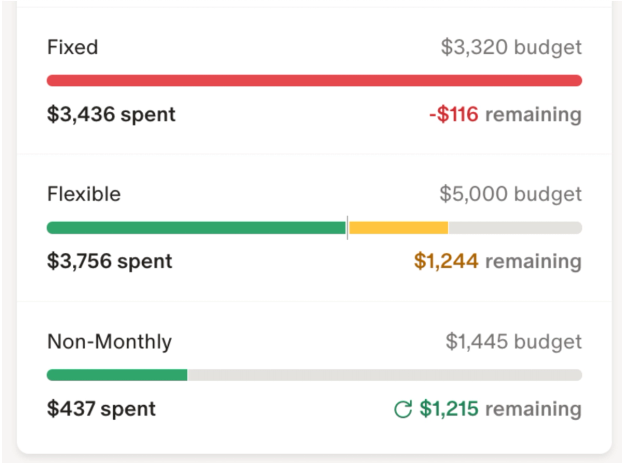

Flex budgeting gives you more workability in your budget by dividing your expenses into three categories: Fixed, Flexible, and Non-monthly.

Fixed expenses are expenses you can expect to pay about the same amount for every month, such as your rent/mortgage, insurance, utilities, subscriptions, debt repayments, and savings/investments.

Flex expenses are your expenses that fluctuate each month. This includes groceries, shopping, entertainment, and other variable expenses.With a flex budget, you don't have to track each one individually; instead you assign a lump sum (also known as your flex number) to your expenses, based on your previous average spending, and stay within the parameters of it.

Non-monthly expenses are large or irregular purchases, such as annual subscription renewals, vacation packages, property tax bills, or otherwise. This way, large purchases don’t mess with your flex number calculations.

What is Category Budgeting?

With category budgeting — the more traditional way of budgeting — you assign every expense category a budget and track your spending at the category level. That means you’ll set a monthly budget for all of your expenses, not just the ones that go up and down each month: rent, utilities, mortgage, taxes, insurance, entertainment, restaurants, clothes, groceries, and more.

Flex vs. Category Budgeting at a Glance

If you need a quick comparison for how flex and category budgets compare, here’s a quick guide.

Flex Budgeting | Category Budgeting | |

How it works | Divide your budget into three buckets: Fixed monthly expenses, flexible/variable expenses, and non-monthly expenses. | Categorize transactions by type, such as Groceries, Utilities, Restaurants, and so on. |

Categories available | Flexible, fixed, and non-monthly | Varies, but generally include utilities, housing, transportation, groceries, restaurants, educational expenses, discretionary shopping, savings, and debt repayments |

Pros | Flexible structure in how you spend your funds Less intensive to plan out with only three categories Allows for achieving goals with some wiggle room in where your money goes | Gives detailed look into transactions Creates a highly structured budget for managing spending Allows for granular control over spending and where your money is going |

Cons | Doesn’t offer as much detail where your money is going Can lack structure with how your cash is spent category-wise Too open-ended and lacking detail for some | Requires more work to build Can be cumbersome to follow with the strict limits Overly rigid and strict if you want a more flexible budget |

Variants | 50/30/20 budgeting, pay yourself first, 60% solution, No-budget budget | Zero-based budgeting, envelope budgeting |

When Flex Budgeting is the Right Choice

Flexible budgeting is all about workability. It’s a more low-effort type of budgeting that works well if you’re not worried about capping spending or getting into the nitty-gritty of your finances. This method might be right for you if:

- You’ve tried other budgets and they didn’t work. Because it gives you one simple number to track and doesn’t require you to reconcile your spending every month or try to use cash for everything, flex budgeting might be the very first system of budgeting that works for you.

- You don’t want to dedicate a ton of time to budgeting. Category budgeting requires more work in terms of setting your categories and your rules, since you have to set parameters for each category. With flex budgeting, all you have to do is set your fixed expenses and your non-monthly expenses, earmark your savings, and let the rest work itself out.

- You don’t want to get into the details of your spending. This is the most common reason someone might choose flex budgeting. Most people are busy, or just don’t have the patience or need to follow every expense in every category. A lightweight way to make sure you’re on track to your goals might be all you need, especially if you consider yourself good with money and generally spend less than you earn. You might find that starting out with flex budgeting gets you excited to go deeper and you decide to dive into category budgeting but you might be just fine staying with your flex number forever.

- Your spending ebbs and flows a lot each month. If your monthly spending varies a lot, it’s more challenging to fit your expenses into the rigid monthly budgets required for category budgeting. You’ll have more variability if you have fairly low fixed monthly costs and a lot of income left over that you can decide to save or spend or if you travel often, have a lot of hobbies or interests, or pay expenses for others (like kids or parents or pets) that you can’t fully control.

- You have big goals you want to save for. When you set up the spending buckets in your flex budget in Monarch, we recommend that you also go to the Goals area of your dashboard as well. There, you can set up and review your bigger financial goals, and then adjust your expenses if you need to. Once you’ve done that, you can be confident that you’ve “set it and forget it” and are saving for your goals without having to nickel and dime every purchase you make.

When Category Budgeting is the Right choice

Category budgeting is all about the details. While it’s more work-intensive, it can offer you some solid insights into how much you’re spending and where your money is going. This method might be right for you if:

- You want to learn about and manage your spending. If you love getting into the details and are interested in managing your spending on specific categories — like eating out, subscriptions, or shopping — category budgeting can help you learn exactly where your money is going and make specific changes.

- You want to track certain expenses for tax purposes. If you make a lot of charitable donations, or if you have a business that you combine with your personal finances, using a category budget will help you keep track of what you can deduct.

- You’re actively trying to cut your spending overall. Setting specific budgets in every expense category can be really helpful to keep on a tighter budget if you need to make cuts. You can also use the category budgeting view to create groups for “needs” and “wants.”

- You prefer to do cash envelope-based budgeting. If you’ve found success with the cash envelope budgeting method (where you take your monthly amounts out in cash and literally put them into envelopes so you know where they’re going), you can set up category budgeting and track your money by adding manual transactions to reflect cash spending.

How Flex and Category Budgeting Compare to Other Popular Methods

There are a multitude of budgeting styles out there, some of which are variants of each style. Here’s a quick summary of some of the most popular types.

- The 50/30/20 rule involves allocating 50% of your budget to needs, 30% to wants, and 20% for savings and investments.

- Zero-based budgeting allocates every dollar to a specific category or purpose, whether it’s saving or spending, making each dollar “work” for you.

- The envelope method allocates exact dollar amounts to “envelope” categories for spending, with a hard cap on spending after the money runs out.

- Pay yourself first/Reverse budgeting saves a portion of your income first before allocating the rest to paying for essentials, and then discretionary expenses.

- 60% Solution (Richard Jenkins) allocates 60% of your spending to committed and essential expenses, like rent and debt repayment, and the remainder is dedicated to savings and “fun” money.

- The no-budget budget automatically saves 10% of your income, while you set essential payments such as rent and utilities on auto-pay and freely spend the rest.

Now that you know the budgeting styles, here’s a quick guide to how they compare with the flex and category budgeting.

Budgeting Types | Flex Budgeting | Category Budgeting |

50/30/20 rule | Allows for flexibility with what your individual needs and wants can be spent on while providing parameters | Can be a useful framework for organizing categories and keeping an eye on overall spending |

Zero-based budgeting | Extremely strict parameters with little to no flexibility | Extremely strict category budgeting, with a higher degree of detail |

Envelope method | More detailed-intensive than a traditional flex budget, but more open-ended than a strict category budget | More open-ended category budgeting with hard caps |

Pay yourself first/Reverse budgeting | Highly open-ended and flexible, with less structure around fixed expenses | Not much structure in terms of categories, and doesn’t offer a ton of detail |

60% Solution (Richard Jenkins) | Similar to flex budgeting, with a more specific percentage assigned to Fixed expenses | More open-ended, and doesn’t offer as much detail as a category budget |

No-budget budget | Similar to flex budgeting, though the auto-pay function allows for less forecasting if your essential payments increase | Doesn’t offer a great deal of detail, since the remainder of your funds are spent freely without regard to tracking |

Combining Flex and Category Budgeting

Flex and category budgeting, while separate philosophies, aren’t complete opposites. If you want a combination of the flexibility a flex budget offers and the detail a category budget offers, it’s entirely possible to combine a flex and a category budget to get the best of both worlds.

How you decide to combine your budgeting styles will depend on your preferences. Here are a few examples of how you can combine the two methods.

- Flexible categories. Instead of going extremely specific on your categories, you can redefine your buckets. So, instead of going with Variable/Fixed/Non-monthly, you can divide your buckets into Needs/Wants/Savings, Housing/Food/Savings/Transportation/Discretionary, or otherwise.

- Fixed needs and savings, flexible wants. Set aside a hard number for your needs, including rent, utilities, groceries, and otherwise based on your previous expenses, along with your savings and debt repayments. The remainder then goes towards your wants, which you can spend on as you please.

- Budgeting with percentages. The 50/30/20 rules is an example of this, where you assign your buckets a percentage of your income instead of a hard number.

How to Set Up Either Method in Monarch

Monarch helps you build a budget that fits your style, with options for both flex and category budgeting available to you. While the default for Monarch is the Flex budget, you can toggle between the two in your budget settings.

Monarch also helps you go beyond simply budgeting. Once you’ve built your budget, you can integrate it into your larger, long-term financial goals such as saving for an emergency fund, building out your retirement fund, paying down debt, and increasing your net worth over time.

Flexible Budgeting

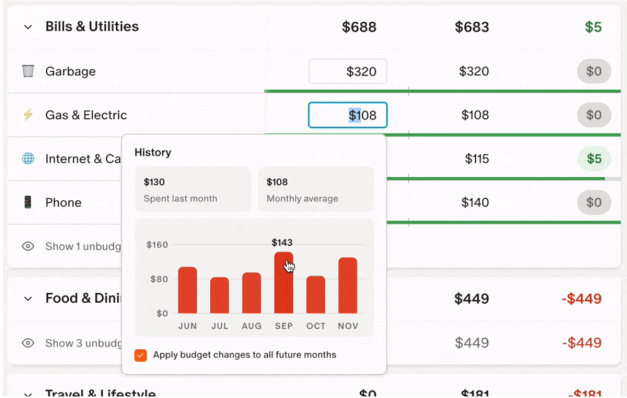

When selecting the Flex budget option, Monarch will group your expenses into Fixed, Flexible, and Non-monthly buckets. Once you’ve linked your spending and savings accounts, Monarch will use your historical data to sort your expenses into these categories, as well as to calculate your flex number. You can go in and toggle your settings as needed.

Once you’ve established your buckets, you can select the text box between each one and edit your budget amount.

Monarch will track your expenditures throughout the month, and alert you if you’ve gone over your category limits.

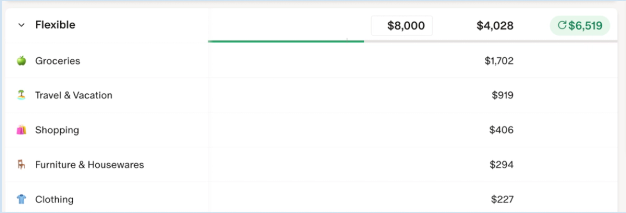

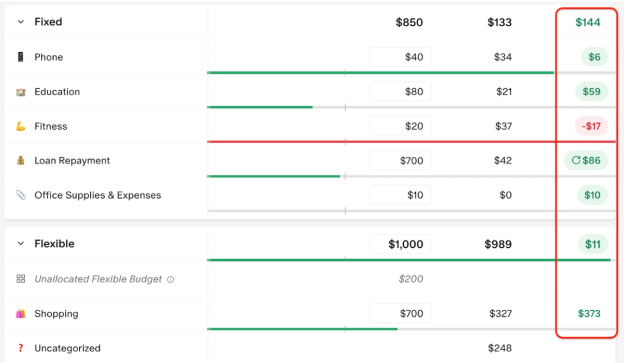

You can also keep an eye on individual category expenditures within your flex budget, and establish individual limits on each category to help you manage spending within your bucket. If you overspend in one category, you can “roll over” cash from other categories if you haven’t yet spent up to the limit.

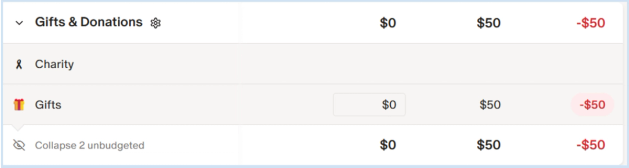

Category Budgeting

When selecting category budgeting, Monarch will have default categories for your transactions. You can review transactions to re-assign categories or tags as needed, based on your preferences. Each category has the option of being assigned a budgeted amount, which you can change at any point. Monarch will suggest how much to budget for each category based on historical data.

Monarch has 60 default categories, which you can choose to disable or rename as needed. You also have the option to add custom categories.

Your categories will be sorted into groups, which you can change and rearrange. Each group will have an overall budgeting number based on how much you budget each category. If you have a transaction for a category you haven’t assigned any money to, that amount will still appear on the category and contribute to the group’s spending total.

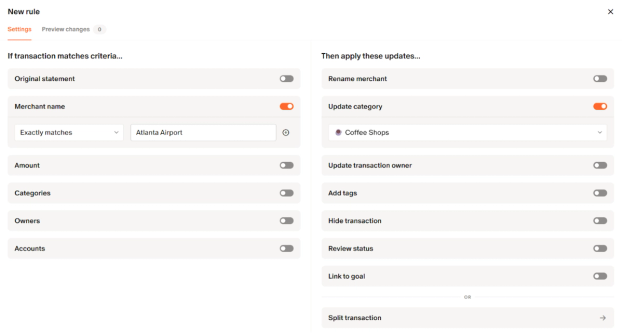

As you spend throughout the month, Monarch will track how your expenses are lining up with your assigned categories, and send alerts if you go over an established limit. You can review transactions to ensure they are being assigned the correct category, and establish rules for which transactions are categorized in what way.

Choosing the Right Budgeting Method for Your Lifestyle

Selecting the right kind of budget for you and your lifestyle will help you achieve financial success. Whether you prefer a simple, workable style that gives you the freedom to move around your money with a flex budget, or a more structured budget with lots of details and limits that a category budget offers, Monarch is there to help you build a budget that works for your style.

With options for both category and flex budgeting, and the ability to customize both to your needs and preferences, Monarch can help you build a budget that fits your lifestyle and that you can incorporate into your overall financial plan for you and your family.

FAQs

Can I switch between flex and category budgeting?

You can. Go to your budget tab, click on “Settings” (the gear icon) and select the budget type of your choice. Then, click “Save.”

How does flex budgeting relate to the 50/30/20 rule?

50/30/20 is a kind of flex budgeting, with your “buckets” being Needs, Wants, and Savings/Investments, with 50% of your income going towards needs, 30% towards wants, and 20% to savings. This allows for flexibility in how you spend your cash, while giving you some hard parameters to work within.

Is category budgeting the same as zero-based budgeting?

While zero-based budgeting is a type of category budgeting, not all category budgets have to be as strict. Some category budgets will leave a bit of wiggle room with income in case of overcharges, or allocate any leftover funds to saving. Zero-based budgeting assigns every dollar to a purpose, making it more rigid, though highly detailed.

Which is better: flex or category budgeting?

That depends on your needs. If you want lots of detail and more fine-tuned control of your spending, then a category budget is better for you. If you want a more flexible budget without as much detail or intensive work, then a flexible budget is better.

How do I calculate my flex number?

Take the previous three months’ of spending in flexible categories, add it up, and divide it by three, which will give you an approximate average to work with. Alternatively, determine how much of a cap you want to put on your flexible spending in order to account for savings, non-monthly expenses and fixed expenses, and work from there.

How do I budget for irregular or non-monthly expenses?

It can be helpful to forecast your budget a few months or a year in advance, so you can account for non-monthly expenses ahead of time, especially if you are aware of a subscription renewal or large expense coming up. Depending on the nature of the expense, you can either cut back on spending for the month or pull from your savings, especially if you have been saving toward a large expense over time. Alternatively, if the expense is unexpected, you can pull from your emergency fund.

What if category budgeting feels overwhelming?

If you’re looking for a place to start with your budgeting and financial management, or want a simpler approach to budgeting, consider trying a flex budget. While it still provides parameters around your spending, it’s not as intensive, and it doesn’t require you to set limits for every single category in your budget.

Does Monarch support both methods?

It does. You can choose between Flex and Category budgeting on your Monarch app, and switch between the two at any point.